(Editor’s note: This is the second part of a two-part series on getting a mortgage in the UK. You can jump to Pt. 1 here.)

After exploring the different types of mortgages available to you, and how much you can borrow, in Pt. 1, you know what you’re looking for. In fact, you might have even found the property that looks right for you. Amazing! So, all that’s left to do is put in an offer, and once it’s accepted, you’re good to go, right?

Of course it’s not that simple. Why do you think there’s a “Pt. 2” in this series, anyway? Putting in an offer is, to paraphrase Winston Churchill ( a man who likely never had a mortgage in his life), not the beginning of the end, but the end of the beginning. So, once you’ve found the property of your dreams and had an offer accepted, what next?

Let’s see:

Beware the hidden costs of “stamp duty”

You may have heard of “stamp duty” on the news and thought it was something to do with the cost of postage (okay, that’s what some of us originally thought …), but it’s actually a cost you’ll have to factor in when purchasing property. Stamp duty is a land tax paid when buying a property above a certain value, with the tax rate depending on the value of the property. It’s higher for those who already own a residential property; second (and third, etc.) homes are taxed an additional 5 percent on top of the existing stamp duty rates.

While there’s no particular processing issue around stamp duty, you’ll need to factor it into your real estate budget. It’s a good idea to calculate what your stamp duty will be before putting in an offer, so you aren’t caught out unawares by additional costs.

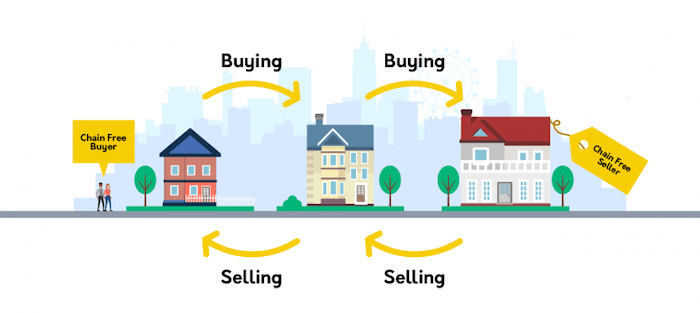

The chain can’t break!

One of the most surprising features of homebuying in the UK, at least from an American perspective, is the concept of “the chain.” When an American is selling their home, they do so with the knowledge that – once they accept an offer – they’ve got to sell up and get out. In the UK, though, it’s a little different.

Many homes for sale in the UK are part of what’s called a “property chain,” where multiple sales are interdependent on each other. This can include things like the current owner of the home you want to buy needing the money from the sale in order to buy a specific home that they are interested in. If they find something wrong with that home (say, the inspection turns up termites in the woodwork), they might back out, and decide to “break” the chain and keep their home. As part of the chain, you’re also a potential “break” in it, so try to get your inspection, financial queries, and more, dealt with before putting in an offer.

The more real estate transactions are involved, the longer the chain. Long property chains sometimes require all involved parties to sign paperwork together on the same day.

Sounds like a bit of a hassle? It can be—some property chains take months to “complete,” meaning for all the interconnected sales involved to go through. You should be aware of this if you’re hoping to move relatively quickly; this may mean prioritizing properties with “no onward chain,” which are less common, but not impossible to find. If a property has just been built, or is being sold by a landlord as opposed to an occupant, it’s less likely to have an onward chain.

Completion day: Getting the keys

So, now is it time to move in? Almost there! The last steps will not be in the hands of the buyers or sellers themselves, but in the hands of both parties’ solicitors. Generally, a solicitor, or real estate lawyer, is required by the bank to get your mortgage. This is to ensure that all complex legal requirements around the mortgage are met. Sellers will often sue solicitors as well for similar reasons. And “completion day” is in the solicitors’ hands. The solicitors will be the ones handling the final monetary transactions between parties to complete the sale.

Once all transactions have gone through, and the money has been transferred, that’s when the chain or the purchase completes. Generally, this will happen between a week or a month after you have personally authorized the purchase. On completion day, the buyer will release the keys to the property and you can collect them. This is timed fairly carefully, as all the keys in a chain are released on the same day—generally, if there’s no chain, you’ll get your keys in the morning, but if you’re at the end of a long chain, it could be as late as the end of the working day for you to receive them.

Phew! After all that —c ongratulations! Once you have the keys, you’re a UK property owner! Enjoy your new home, and happy moving!

–––––––––––

Read more about the UK here in Dispatches’ archives.

Ellery Weil

Dr. Ellery Weil is a writer and historian based in London. She was born in Washington, DC, raised in Maryland, and attended undergrad in Ann Arbor, Michigan, before moving to the UK to attend grad school at University College London, where she earned her PhD in History. She lives in London with her husband, where you can find her writing, reading, petting dogs in Regent's Park, and exploring the city's antique markets.