The days are shorter. Shoes are being set out for Saint Nicholas. Christmas trees are being decorated. Presents are being bought. But Dutch residents have something a little less festive on their to-do list before they can completely enjoy the season worry-free: Choosing health insurance for next year.

That’s right, every year Dutch residents have the choice to change their health insurance for the following calendar year.

This means changing providers, upgrading a plan by adding coverage, downgrading (yes, this is a thing) or changing the deductible.

Choosing a plan

To start at the basics, every Dutch resident is required to have basic health insurance. It’s a privatized system but each insurance company must offer a standard, universal plan that is similar in price regardless of age or existing health conditions. Residents can increase this plan if they choose.

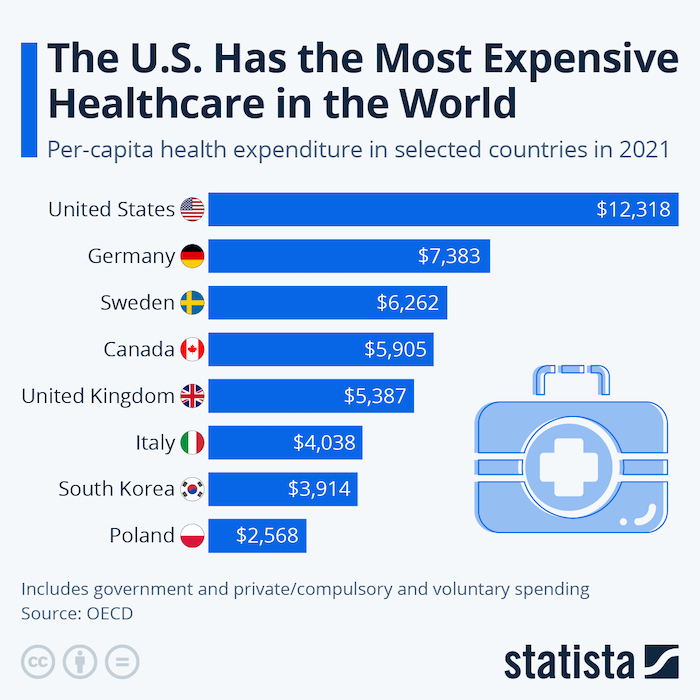

In November, I received my premium for 2025 and it went up 6 percent, or 9 euros per month. I’ll pay a little over 155 euros per month, which compared to countries such as the United States is a fraction of the cost, especially when you consider that the price covers me and my children. (Children under 18 are free except for things like orthodontics).

For someone who doesn’t expect changes to my health or additional procedures, I’ll probably keep mine the same. But in previous years, I’ve added coverage, like dental care and a premium international module to cover more costs abroad.

Everyone should take a careful look at their current plan and make sure they are best covered for the coming year.

Why would you want to change your health plan?

Have you had major changes in your health this year? Are you expecting to have a major procedure like a colonoscopy? Are you pregnant?

These could be reasons to change your health insurance plan in the coming year. This is a minor way to game the system by changing a plan from year to year. If you predict major health costs, especially hospital procedures, then you might want to lower your deductible or add other modules to your plan.

When I was pregnant, I found out the calendar year before. September to December are the worst months to have a baby because you don’t have the opportunity to change your health insurance to a more premium one beforehand. I had the most basic insurance for years before I got pregnant, so I decided to upgrade so it covered the entire cost of a hospital birth and post-birth maternity care at home.

Let’s be honest; we are not talking thousands of euros here.

In the Netherlands, a hospital birth is a maximum of 580 euros in 2025 if you don’t have a medical necessity. Many other situations are similar because Dutch health care costs usually won’t break the bank.

Whatever your situation is, revisit your health insurance and double-check that you have enough coverage.

Here are some helpful tips:

• Use price comparison via websites like Independer and Zorgkiezer

These sites help to see the options available, but keep a close eye on what each plan covers.

• Make sure the plan covers your nearest hospital

Imagine you need to go to the emergency room or have a planned medical procedure. Will you want to travel to a hospital farther away for medical care? I know it sounds weird, but this is a quirk of the Dutch insurance system. Some of the standard plans do not cover every Dutch hospital because each insurance company negotiates with the hospitals on which ones are covered.

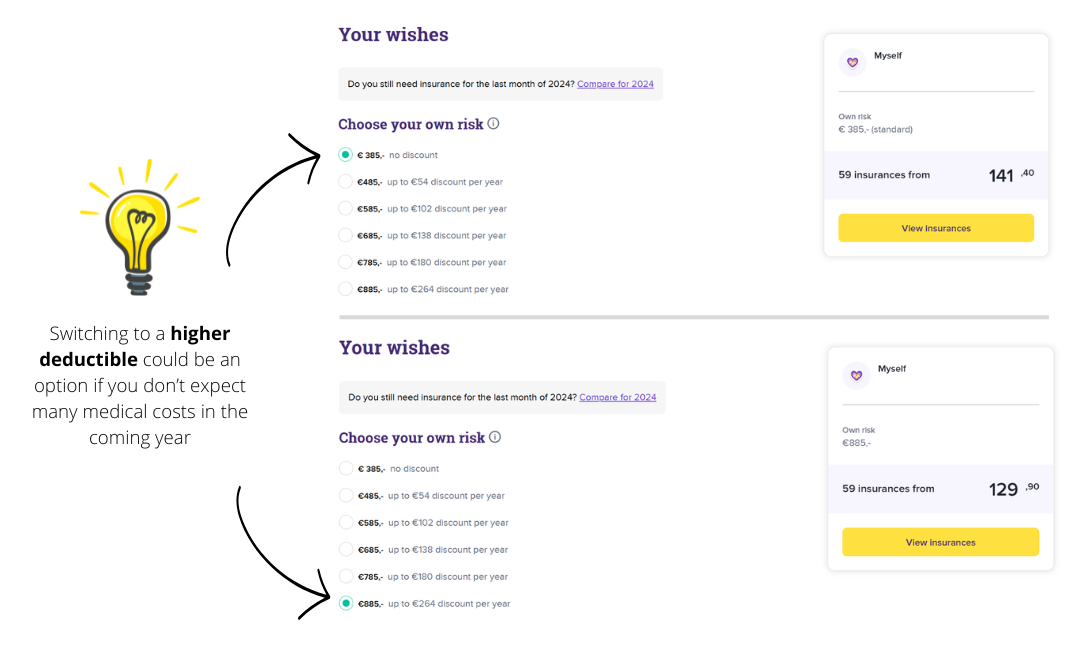

• Consider increasing your deductible

I know what you’re thinking … why would you want to ever increase your deductible? In some cases, though, it could be worth it. Choosing a higher deductible could be an option if you don’t expect many medical costs in the coming year, as I show in the graphic below.

In the example above, you can save 11.50 euros per month (138 euros per year) by choosing the higher deductible. The risk? If you have many medical expenses that hit the deductible, you could end up paying 362 euros more for the year.

It’s all based on how much risk you want to accept.

In my personal experience, I’ve selected the highest deductible (885 euros) since 2020. In exchange for accepting more risk, I’ve paid a lower premium each month in return. In my case, it has worked out so far and I calculate that I have saved a total of 600 euros over these five years.

I’ve paid 109 euros on average per year in out-of-pocket expenses.

What you can’t see from the average above is that I paid 400 euros last year for ER visits related to a bad case of pneumonia. Hospital visits are not completely covered even with a referral, as in my case. It comes out of the deductible. However, I paid hardly any out-of-pocket costs in the years prior.

That goes to show that you can’t predict your health, but I still only paid 16 euros over the lowest available deductible in 2024. With a low deductible, you are guaranteed to pay every month via your premium, while with a higher deductible, you just “might” pay. Do the math and find out what’s best for you.

• Know what your travel coverage will be for health emergencies

You can’t choose when you get sick and if you are an expat, you need to make sure you are covered for health emergencies, especially if you travel to the U.S.

If you live in the Netherlands, the standard plan covers international medical costs at the equivalent Dutch prices. This will usually be fine in many other countries, including Europe, but if you end up with an emergency in the U.S., it could spell financial ruin. (Yes, I’m serious.)

I choose to pay more each year so medical expenses abroad are covered at the foreign rates. For me, this is non-negotiable as an American expat.

Check out my story here about ending up in an American emergency room with my young child.

Not perfect, but compared to the US ….

The Dutch healthcare system has its quirks and frustrations, from its laissez-faire attitude about prescribing medicine to finding out your nearest hospital may not be covered by your plan. Expats love to complain and each person seems to have a crazy story about how the system failed them. It’s true, it happens, but I’ve also found many proactive doctors who treated my family for serious issues.

I tend to forgive the system given how little I pay compared to the U.S. No system is without flaws and the Dutch system has its flaws. Your health is important and that starts with making an educated choice for a health insurance package that fits you and your family.

Remember, you have until the last day of the year to make any changes. Believe me, I know someone who was on the phone on 31 December with customer service, but I don’t recommend it! Do it now and cross it off your to-do list.

Happy holidays and good luck making your choice. Worst comes to worst, you can choose again next year.

Lane Henry is an accidental long-term expat. She is an American who came to the Netherlands for two years—or so she thought. She has now lived in the Netherlands and explored Europe for over a decade.