Credit card fees on foreign transactions … they’re the bane of expats, techpats and pretty much anyone who travels overseas regularly. The good news is that if you’re holding a credit card issued by a U.S.-based bank while living or traveling in Europe, you’ll increasingly be spared the foreign transaction fee on every purchase.

That’s the assessment of the website CreditCards.com, which recently surveyed the 100 most popular cards. “Right now, 61 of those still charge foreign transaction fees,” says Matt Schulz, the site’s senior industry analyst. “A year ago, 77 of the 100 were levying those charges.”

And since this is such a “copycat business,” says Schulz, “more and more U.S. banks are likely to fall in line.”

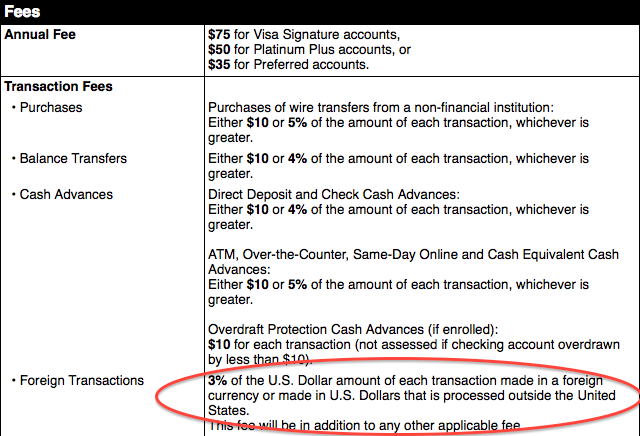

Such fees can add up to 3 percent to purchases … no insignificant amount when you charge, say, two weeks at a resort, rental cars, a watch, jewelry or high-end apparel. And in the bad old days, banks used to go out of their way to hide them … until they lost a class-action suit back in 1996.

Such fees can add up to 3 percent to purchases … no insignificant amount when you charge, say, two weeks at a resort, rental cars, a watch, jewelry or high-end apparel. And in the bad old days, banks used to go out of their way to hide them … until they lost a class-action suit back in 1996.

Schulz says the trend is being driven not by banks’ concerns for overloaded, overcharged cardholders (you didn’t really think that, did you?) but by shrewd assessments of the marketplace. “International travelers tend to be the more upscale part of the population, people who will charge a lot of larger purchases, and that’s the customer banks want to attract,” Schulz says. “One obvious way to attract this group is by eliminating the fees on foreign transactions.”

Originally, says Schulz, the fee was levied to help banks cover the costs of managing the currency exchange fluctuations for purchases made in pounds or euros, but charged to the cardholder in dollars. “But they’ve seen that the value of eliminating the fee outweighed the costs of the exchange,” he says. “If the banks thought they’d make more money with the fee, they’d have kept the fee.”

So which are the credit cards that have eliminated the foreign transaction fees? And which, by the way, are the best cards for Americans to carry when abroad? CreditCards.com makes the following recommendations:

- Capital One Quicksilver Cash Rewards

- BankAmericard Travel Reward

- Chase Sapphire Preferred

- Capital One Venture Rewards

- Capital One VentureOne Rewards

- Alaska Airlines Visa Signature

- Capital One QuicksilverOne Cash Rewards

- Discover It Cashback Match

- Premier Rewards Gold from American Express

- MasterCard Titanium

CreditCards.com is not the only website providing advice on choosing the right credit card. Other sites include:

- NerdWallet.com

- MoneyUnder30.com

- WalletHub.com

- NomadicMatt.com

- Investopedia.com

And the travel-abroad card that seems to rank at or near the top of nearly everyone’s list is Chase Sapphire Preferred, which – says NerdWallet – “offers one of the best sign-up bonuses in the business: earn 50,000 bonus points when you spend $4,000 on purchases in the first 3 months from account opening. That’s $625 in travel when you redeem through Chase Ultimate Rewards.”

NerdWallet also praises Chase Sapphire Preferred’s two Ultimate Rewards Points per $1 spent on travel and restaurants, and one point per $1 spent elsewhere; its high redemption value (points are worth 25 percent more if you redeem for travel booked through Chase’s tool); a favorable 1:1 ratio if you transfer your points to an approved travel partner; a zero-dollar introductory fee for the first year; a $95 annual fee thereafter “pretty reasonable for such a high-earning card.”

And, of course, no foreign transaction fees.

By the way, CreditCards.com also operates the site uk.creditcards.com, which evaluates the best credit cards issued by British banks.

These days, it likes:

- Virgin 41 Month Balance Transfer;

- the MBNA Platinum Credit Card;

- the Tesco Bank Clubcard for Balance Transfers;

- Aqua Classic;

- Capitol One Classic Platinum MasterCard;

- and the Ocean Credit Card.

Now for the bad news:

As we’ve told you previously, Americans living abroad – rather than just traveling – have a much bigger challenge than simply finding the best U.S. bank-issued credit card or the one that doesn’t charge foreign transaction fees.

A variety of international agreements, bank policies on both sides of the ocean and all those annoying terrorist activities have combined to make it next-to-impossible for American expats to open bank accounts in Europe. And that includes getting a credit card from a European bank or keeping and using the credit card you had with the American bank.

Schulz acknowledges the problem, recommending that “the best thing is probably to keep using a U.S. address, perhaps that of a friend or relative.” Not as easy as it sounds, banks can sometimes be as smart as you or me.

The article posted on DispatchesEurope on June 13, 2016 (“Dispatches’ foolproof solutions for overseas banking hassles”) offers a few good recommendations, such as European banks like HSBC, that cater to expats – and charge mightily for the service; American Citizens Abroad, which has made arrangements with the U.S. State Department Federal Credit Union, the one that serves Americans working at U.S. embassies, among others; and Monese, the digital financial services institution.