(Editor’s note: This post is an edited version of Tranio’s findings from its latest real estate survey, which found that Russian-speaking real estate investors are seeking investments that also include European residency, or at least the possibility of gaining a passport. You can read the full report here on Tranio. Rostislav Chebykin, Tranio editor-in-chief, is author of the report.)

The opportunity to acquire foreign residency proved to be the key driver encouraging Russian-speaking investors to scoop up properties abroad, according to our latest poll. Toward this end, these investors have exhibited a preference for purchasing residential properties, followed by hotels, retail properties and land plots.

The average transaction budget among our respondents was 620,000 euros – a figure that has doubled since our 2019 survey – although particular budgets vary from 180,000 euros to 3 million euros by country. On average, Russian-speaking investors expect a net ROI of about 5 percent per annum from their core rental business.

Key drivers: residency, capital preservation, and capital increase

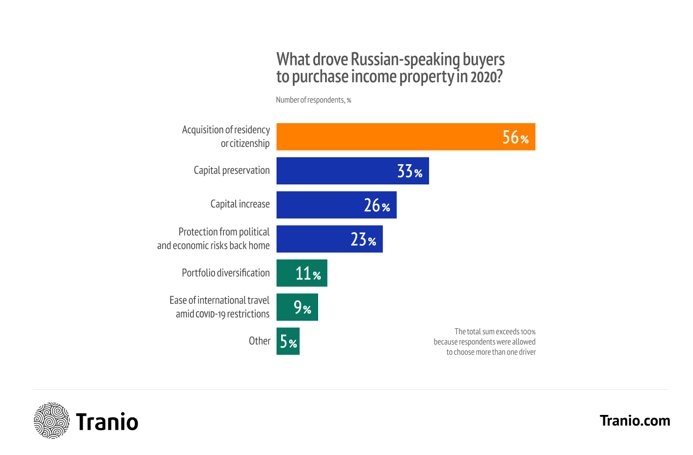

Nearly half of our respondents (48 percent) said their clients from Russia and the Commonwealth of Independent States countries were primarily interested in the acquisition of residency or citizenship with purchasing income properties in 2020.

Tranio’s Marina Filichkin

None of the other drivers on the list was chosen by more than one-third of the respondents.

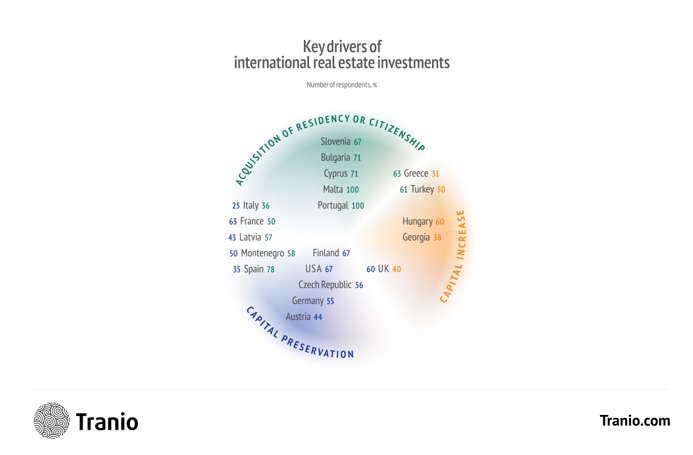

Surprisingly, many respondents cited residency as a driver even in the countries where residency is not an immediate option in connection with the investments. Residency is a more obvious driver for investments in countries with residency- or citizenship-by-investment programs (i.e. Greece, Spain, Portugal); but this was also a key motivator in countries offering golden visas for investment in assets other than real estate (specified by 71 percent respondents in Bulgaria and 36 percent of respondents in Italy), or even in countries that do not offer residency by investment (named by 67 percent of respondents in Slovenia and 50 percent in France).

George Kachmazov, Managing Partner at Tranio, believes these conclusions reflect a long-game approach to property investments. “These findings can be interpreted as identifying not only the investors that immediately acquire their golden visas, but also those who purchase properties as part of their wider investment activities ultimately targeting naturalisation in a foreign country.

“To illustrate, many wealthy Russians plan to spend their retirement years on the Côte d’Azur or other luxury locations in France, so they are now building up their business and personal presence there to facilitate acquisition of residency in the future,” Kachmazov said.

The acquisition of residency or citizenship is a key driver for international real estate investors in this demographic.

Portugal and Malta attract investors by residency, while Finland and the USA – by capital preservation

Buyers targeting the most popular countries choose one or two of the three key drivers: acquisition of residency, capital preservation, or capital increase.

“The predominance of one driver – such as golden visas – in a particular country does not imply that such a country would be an inappropriate choice for other types of investments,” Kachmazov said. “There are quality projects geared toward capital preservation as well as capital increase in all the 64 countries where we work.”

Half of respondents from Georgia said the key investors’ driver was “Protection from political and economic risks back home”. While rare in other countries, this factor proved to be a second-place driver for Germany (43 percent) and the USA (33 percent).

Investment portfolio diversification was important for Russian-speaking investors in Slovenia (33 percent), Latvia (29 percent), Austria (22 percent), and the Czech Republic (22 percent).

The driver “Ease of international travel” did not factor among the top three drivers for any of the countries but received notable scores for investors in France and Montenegro (chosen by 25 percent respondents for each of these countries) and Greece (19 percent).

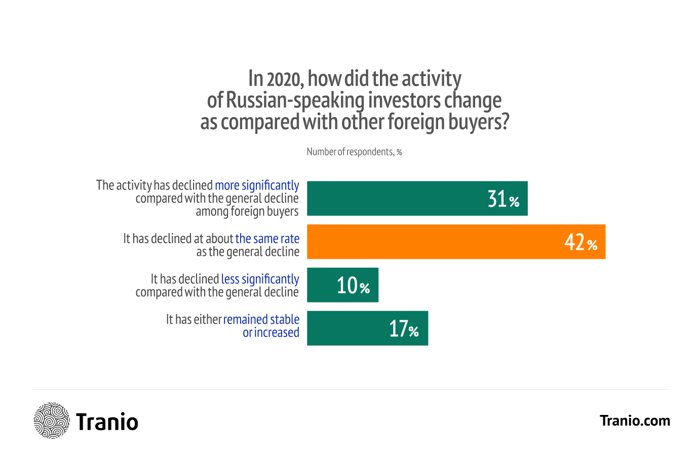

The United Kingdom is the only country surveyed where Russian-speaking investors were more active in 2020 than they had been previously

In 2020, Russian-speaking investors abroad were sluggish compared to previous years, but were no less active than investors from other countries, according to 42 percent of respondents. However, another 31 percent of respondents said that activity had declined much more.

The survey findings produced tentative estimates of rates of increase or decrease in activity by Russian-speaking investors as compared with general international dynamics:

- Their activity declined by 15-20 percent compared with the other foreign investors in countries for which the predominant driver was residency. Major declines were seen in Italy and Spain (by about 30 percent each), Austria (by 40 percent) and Bulgaria (by over 50 percent).

- The activity of Russian-speaking investors declined at a similar rate to that seen among other foreign buyers in countries targeted mostly for capital preservation.

- In countries that tend to attract investors driven by the goal of increasing capital, investment activities fell by 10-15 percent as compared to other foreign investors. The decline in Turkey was only about half as pronounced as that seen among others, and the UK is the only country named by the respondents where Russian-speaking investors showed more activity in 2020 than before.

The UK is the only country named by the respondents where Russian-speaking investors were more active in 2020 than before.

In comments accompanying their responses, respondents suggested that much of the decline in activity in 2020 was attributable to investors with low budgets, whereas high-budget investors continued to channel their funds much as they had previously. The respondents observed highly pent-up demand in some countries (e.g. Germany) and expect the market to rebound powerfully as borders reopen.

Demand for housing fell by more than 20 percent

Forty-four percent of respondents believe that demand for residential properties among Russian-speaking buyers fell by more than 20 percent in 2020, compared with 2019.

This is characteristic for most of the countries, with a few notable exceptions:

- Demand in Austria, Czech Republic, Greece and Montenegro fell less harshly by 10-20 percent.

- On the contrary, demand for residential housing increased by about 2.5 percent in the UK and by 4 percent in the USA.

Demand for residential properties among Russian-speaking buyers fell precipitously.

Demand in countries primarily targeted for residency fell most markedly by 21 percent on average. By comparison, countries that typically attract investors motivated by capital preservation or increase only saw activity fall by some 15 percent.

This decrease in demand for residential real estate abroad is corroborated by Tranio sales statistics: Tranio closed 30-percent fewer deals in the residential segment in 2020 as compared with 2019.

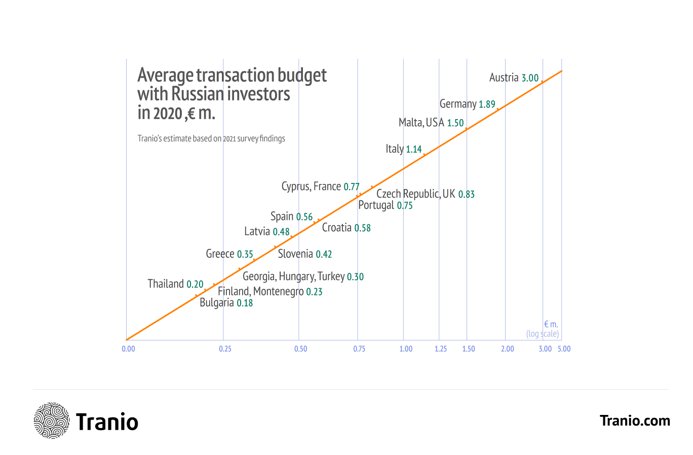

The average investment budget in 2020 doubled

The average transaction budget among Russian-speaking investors in 2020 was 620,000 euros, more than twice as much as that of 2019 (300,000 euros). Some 73 percent of respondents specified a budget of up to 1 million euros.

The budget is especially high in countries for which the key driver is capital preservation, in which case average transaction amounts reach 830,000 euros. In countries where investors are focused on capital increases, the situation is the opposite: the average budget was as low as 300,000 euros.

The average budget in the countries chosen for the purposes of residency is 520,000 euros.

Austria stands out clearly against the general backdrop with an average budget of 3 million euros, and Bulgaria and Thailand turned out to be the cheapest countries with budgets of 180,000 euros and 200,000 euros, respectively.

Investors reduced their yield expectations for core rental businesses to 5 percent per annum – down from 6.7 percent

In 2020, Russian-speaking investors expected an average net ROI of 5 percent in core rental projects, whereas the average expected net ROI was 6.7 percent just two years ago (based on Tranio 2018 survey findings).

Generally, investors did not expect a net ROI of less than 4 percent in any of the countries surveyed. Investors’ appetites were most modest in Portugal, where the standard expectation was 4.25 percent, as well as in the UK and France (4.5 percent in each). Expected ROIs remained highest at 5.5 percent and up in Hungary, Cyprus, Latvia, Slovenia, the USA, Thailand, Croatia, and Montenegro.

In 2020, Russian-speaking investors expected an average net ROI of 5 percent in core rental projects.

It is fair to assume that investors expect higher yields in countries delivering capital increases, but the survey findings speak to the opposite: the expected net ROI is 4.74 percent in countries sought out for capital increase compared with 4.88 percent in the countries sought out for capital preservation, and 4.95 percent in countries targeted for residency. As Kachmazov explains, “The investors serious about pursuing capital increase are usually more experienced; as such, their expectations are comparatively moderate and accurate.”

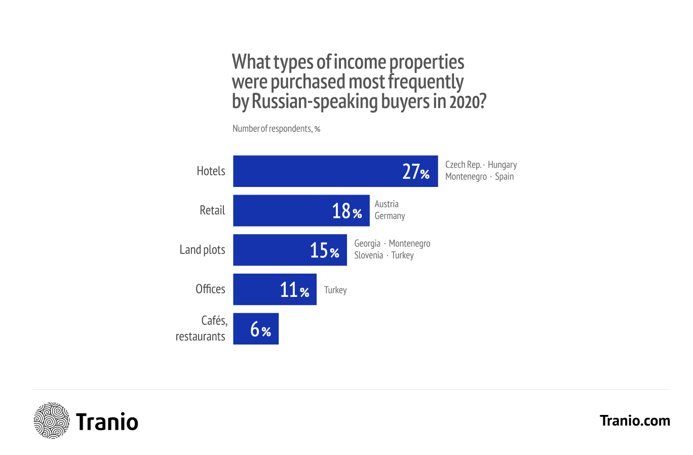

Hotels, land plots, and retail properties proved to be the most popular types of commercial property.

Survey respondents believe that in 2020, apart from residential properties Russian-speaking buyers invested abroad primarily in hotels, retail properties (shops, supermarkets, shopping centres, etc.), and developable land.

Other types of income property with less than 5 percent response rate comprise warehouses, industrial real estate, hospitals and senior care facilities, gas stations and car parks.

In 2020, Russian-speaking buyers invested abroad primarily in such commercial property types as hotels, retail, and developable land plots..

It might seem strange that hotels have proven popular amid the radical travel reduction, yet Kachmazov explains, “Hotels have become more affordable amid the lockdowns, and that might be the point. Russian investors are taking advantage of the situation to invest in such assets.”

The respondents commented that the buyers were especially interested in tenant-occupied properties, preferably with guaranteed long-term lease contracts.

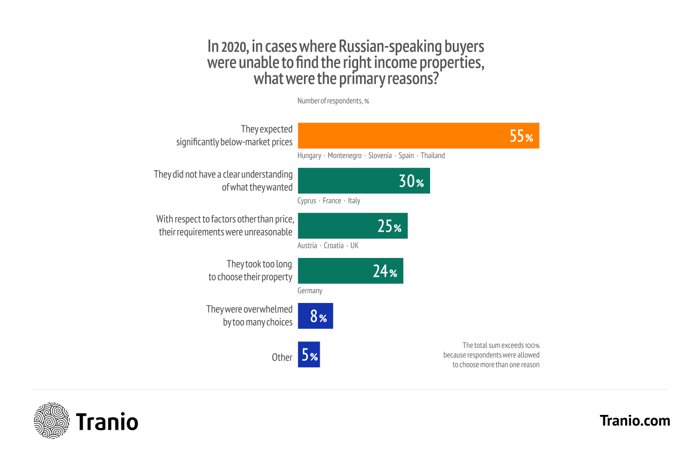

Investors expect significantly below-market prices

Respondents to Tranio’s previous surveys noted that Russian-speaking investors often failed to find or select suitable properties. More than half – 55 percent – of respondents named property selection as the most difficult step when purchasing properties in 2017, and the same search and selection issues were the main reasons for transactions having fallen through in 2018 and 2019, according to 26 percent and 29 percent respondents respectively.

Tranio asked respondents to clarify in the 2021 survey what particular difficulties were encountered when looking for and selecting the property. According to the majority of respondents (55 percent), the key reason for failure was that investors expected significantly below-market prices for their properties. This is the most common answer for almost all countries.

Price issues proved to be relatively uncommon in countries where investors are driven by capital preservation than elsewhere (50 percent of respondents specified this issue, on average). A lack of clear understanding of what investors wanted was less topical for countries sought out for capital preservation or capital increase, and remarkably, no respondents chose the phenomenon of being spoilt for choice as a problem in such locations.

Investors fail to find or select appropriate properties primarily because they expect significantly below-market prices.

On the contrary, expectations far from the market realities (other than the price) are more common in countries targeted for capital preservation or capital increase (28 percent of respondents) and less common in countries targeted for residency (21 percent).

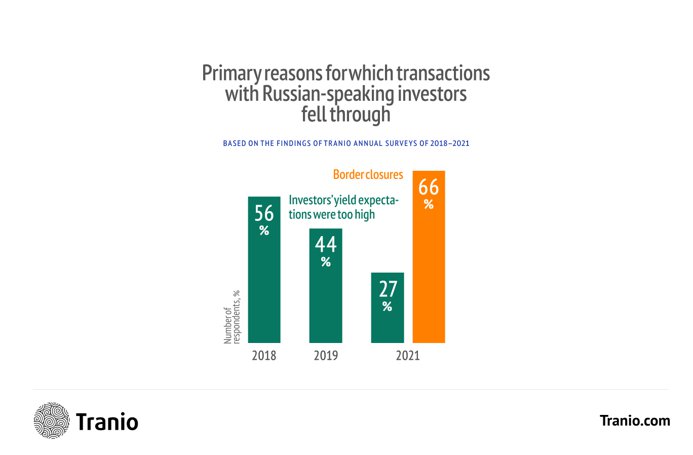

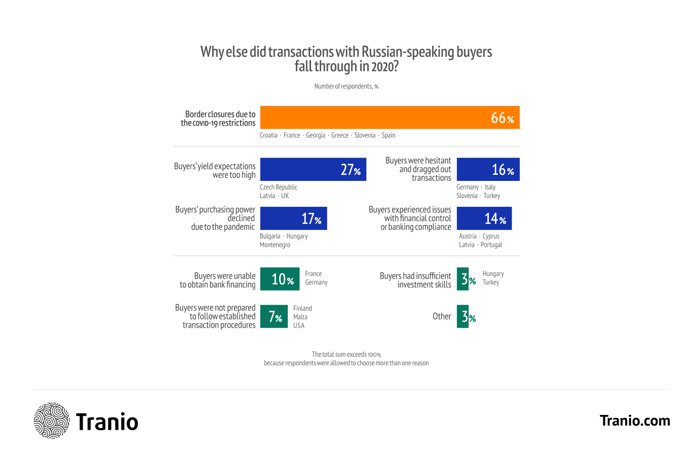

International travel restrictions were a key cause of transaction failures, but they were not the only factor

International travel restrictions were the top reason for transactions having fallen through in 2020, according to 66 percent of respondents. This fell into the top two causes for such transaction failures in all countries we considered, having received especially high response rates in Georgia (100 percent), Slovenia (83 percent), Croatia (80 percent), Greece (76 percent), Spain and France (75 percent each). It bears noting that border closures proved to be an issue for real estate professionals in countries where investors were primarily driven to obtain residency or citizenship through their investments.

Financial control and banking compliance, rather than travel turned out to be the top issue in some countries, such as Latvia (67 percent of respondents), Austria (57 percent), Cyprus (50 percent), and Portugal (36 percent). It is noteworthy that most of the respondents in all of these countries also mentioned excessive yield expectations.

Generally, inflated yield expectations are the most common problem for countries where investors target capital preservation or capital increase. It is the top issue in the UK (75 percent) and the Czech Republic (57 percent).

Border closures have proven especially problematic for real estate professionals in countries where investors expect to obtain residency or citizenship.

The reason that investors were hesitant and dragged out transactions was especially marked in Slovenia (33 percent of respondents), Germany (32 percent), and Italy (22 percent). The fact that the buyers were not prepared to follow established transaction procedures proved the top one reason for transaction failures in Malta (67 percent) and the second leading reason in the USA (25 percent). The answer “Their purchasing power declined due to the pandemic” was especially pertinent for Bulgaria (57 percent) and Montenegro (38 percent).

Issues with obtaining a bank loan had a high response rate in countries people targeted for capital preservation (e.g. 21 percent of respondents in Germany) and were not noted at all in the countries targeted for capital increase (the UK, Hungary, Georgia).

The survey findings unveil a paradoxical trend: the lower the average transaction budget is in a particular country, the more topical the reason “Their purchasing power declined.” To illustrate, this reason was noted by maximum respondents in Bulgaria (57 percent) where the average budget is the lowest (180,000 euros). On the contrary, in Austria which is in the opposite pricing category (with an average budget of 3 million euros), no respondent selected that reason.

A paradoxical trend: the cheaper a particular country is, the more topical the reason that purchasing power of buyers declined is in it.

During the history of Tranio annual surveys (since 2012), we have observed the same typical issues encountered by Russian-speaking investors. However, two struggles have been and remain major during all these years: Russian-speaking investors expect significantly below-market prices and net ROI materially above the real yield.

Tranio is a Moscow-base broker with offices in Bryansk, Spain (Barcelona, Alicante, Torrevieja) and Germany (Freiburg). More than 11,000 people per day visit the Tranio website, and the company’s revenue grew by 18 percent in the past year. In 2017, 26 percent of all the company’s transactions involved foreign clients. In particular, Tranio closed several large commercial real estate transactions in Germany to nationals of Pakistan, Turkey and South Africa.

See more Tranio research here.

Read more about real estate across Europe here on Dispatches.