When I first started visiting the Netherlands, everyone seemed to want to ask me about Brexit. By the time I had moved here, in the final months of the negotiations towards a deal/no deal, I was regularly quizzed on the latest events in the ever-changing saga. A few times I was tempted to say, hold on, I’ll just ring my hot-line to Boris and ask him what’s happening. The truth was, I was glad to leave behind something that had dominated the national psyche for so long.

I was genuinely surprised, however, just how much of the daily developments and political wrangling was followed closely along by our European neighbours. They were well aware of every detail and its potential impact. It was only then that I began to understand how, as a British person, I had viewed Brexit as something that affects the United Kingdom, something we have done to ourselves. Understanding the impacts from a European neighbour’s point of view is another thing entirely, and while the UK is still going around in circles supposedly negotiating on a deal at the 11th hour, the rest of Europe has moved on and made their plans without us factored into them.

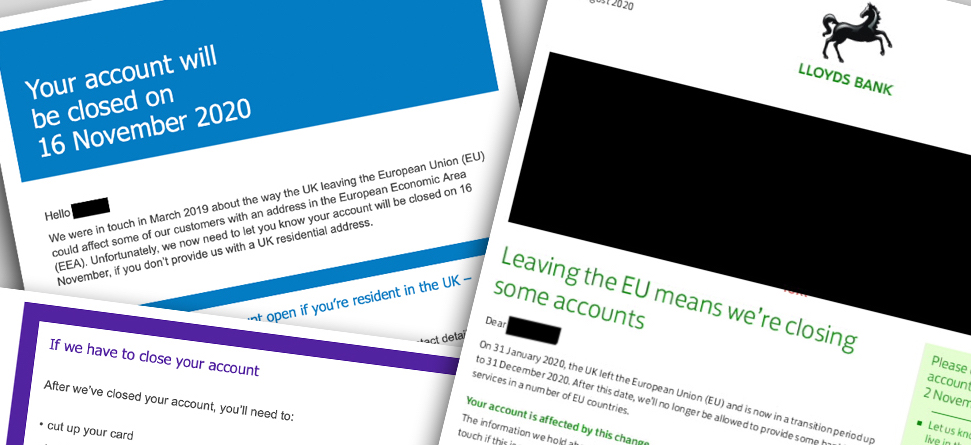

Lloyds closes my account

So far, the only immediate impacts for me here in the Netherlands have been securing a residency card and swopping my British driving licence for a Dutch one. Both of these processes were straightforward. Things were not quite so smooth from the British side, however. On 28 August, I received a letter from my UK bank, Lloyds, stating that as a result of the UK leaving the EU, some bank accounts (for people who didn’t reside in the UK) would have to close.

This opened up a whole rabbit-hole of research into banking options for those who needed to keep a UK bank account, in Pound sterling, for whatever reason, but who reside elsewhere. A newly-found Facebook group, British Expats in the Netherlands, revealed that in terms of high-street banks, the only option was HSBC. As an international bank, they allow UK accounts with EU addresses.

Others were offering this but are closing down this offer to new accounts. I got straight onto it and started the application process.

Here I am, more than three months later, with no account open (although repeated phone calls to HSBC assure me it will be processed soon …)

HSBC’s service to open an account online seemed to stop once the initial online form had been filled in. In the past three months, aside from taking a screenshot of the original “your application has been successful” information, I have had no letters, emails or any other contact from HSBC.

All contact has been from me, calling repeatedly. I have posted through the proof of identification and address required, witnessed by a solicitor (called a “notary” here). This wasn’t accepted, as my notary used a company stamp and signature rather than hand-writing the exact words.

My crazy paper chase

My mistake, so I tried again.

This time I thought I’d take no chances – I hopped on a plane, armed with ID and four examples of proof of address (I only needed one), and visited a branch. I was told they couldn’t help me. They weren’t allowed to open accounts at the branch due to COVID-19. I was a bit upset having travelled a long way and having called the previous week and being assured I could go into any branch, without an appointment and open an account. All they could do was take my documents and scan them through to the team handling my original account request.

The cashier took a look at my documents and discounted all of them.

They wouldn’t accept a bank statement from my Dutch bank, as it was in Dutch. I’d figured a document that was mostly numbers didn’t need translating anyway. Just in case, I’d brought along a letter in English from my Dutch bank. That was discounted too, as it had a disclaimer at the bottom of it. My other documents were discounted as well.

I mentioned why I was there, as my Lloyds account was closing, and the cashier suggested I go to Lloyds and get a statement from them.

I did, and thought I was clear. The following week, when chasing up on the phone, I was told they did not accept statements that had been printed out in branch (or at home). Others in the Facebook group had had similar experiences. One lady’s bank statement as proof of address was rejected because her notary had not signed each of the 10 additional pages.

Back to square one.

My final attempt involved posting more proof of address documents, this time via a British solicitor to be verified – seems to have worked.

The customer experience trying to open an account, from another country, via post, is challenging to say the least, and in stark contrast to the experience opening an internet-only bank account – which I had considered as a solution for my banking needs.

Can the internet-only banks save the day?

Find out in Pt. 2 coming up.

You can see all of Dispatches’ Brexit posts here.

About the author:

Rachel Arts originally is from the UK but relocated to Eindhoven in 2019 with her husband. Rachel is an entrepreneur. Her business, Talentstorm, draws on her 20-plus years in corporate learning to help develop individuals and organisations.

She loves to write about all things to do with personal development, self-directed learning and modern learning practices. To learn more more, check out the Talentstorm website here or follow her people-development blog here for regular tips to achieve work and career goals.